Collateral-Based vs. Non-Collateral-Based Private Placement Programs (PPPs)

Private Placement Programs (PPPs) offer a range of investment opportunities, and one of the key distinctions between these programs is whether they are collateral-based or non-collateral-based. Understanding the difference between these two structures is critical for investors when deciding which type of PPP best aligns with their investment goals, risk tolerance, and desired level of security.

What is a Collateral-Based PPP?

A collateral-based PPP requires investors to pledge collateral, which could be in the form of cash, precious metals, securities, or other assets to secure their investment. This collateral acts as a form of protection for both the investor and the program, ensuring that there is a backup in case the investment doesn’t perform as expected.

Key Features of Collateral-Based PPPs:

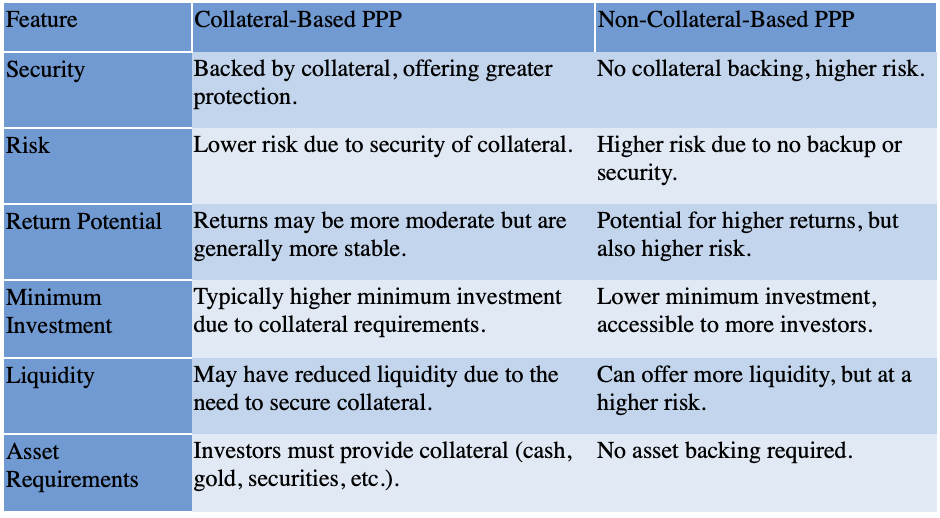

- Security: The collateral provides an added layer of protection for the investor. If the investment fails or the program doesn’t deliver the expected returns, the investor’s collateral can be used to recover the lost funds. This offers a level of risk mitigation.

- Lower Risk: Because the program is backed by tangible assets, collateral-based PPPs tend to be less risky than their non-collateral-based counterparts. The presence of collateral helps to reassure investors that their capital is somewhat protected.

- Collateral Options: Depending on the program, the collateral can be in various forms such as cash, gold, real estate, or even other securities. The choice of collateral can influence the risk profile and return potential of the investment.

- Higher Minimum Investment: Since collateral is involved, investors may need to commit a larger minimum investment to participate in collateral-based PPPs. This can be a barrier for some investors but provides more security for those who are able to invest larger amounts.

- Liquidity Risk: If the collateralised asset is illiquid, it may be difficult to quickly convert it into cash.

- Valuation Risks: Accurately valuing collateral can be challenging, especially in volatile markets.

How It Works:

- The investor provides collateral (such as cash, gold, or other securities) to participate in the PPP. This collateral is held by a trusted intermediary or the platform itself.

- If the investor’s position is at risk or the program experiences issues, the collateral can be liquidated to cover potential losses.

Benefits:

- Security: Investors are generally protected against losses to some extent, as the collateral serves as a buffer.

- Lower Risk: The requirement for collateral often reduces the chance of fraud or total loss, providing more assurance for investors.

Risks:

- Capital Lock-Up: The investor’s collateral is tied up for the duration of the program, limiting access to those funds for other investments.

- Collateral Value Fluctuations: If the collateral’s value decreases (e.g., in the case of volatile assets like gold or stocks), investors might face losses despite having provided security.

Example of a Collateral-Based PPP:

If you invest $100,000 into a collateral-based PPP with a collateral requirement of 30%, you would need to provide $30,000 worth of assets (e.g., cash or gold) as collateral. If the program doesn’t meet expectations, the collateral would be used to cover some or all of the loss.

What is a Non-Collateral-Based PPP?

A non-collateral-based PPP, on the other hand, does not require investors to provide any collateral to participate. The investment is unsecured, and investors are placing their capital solely on the creditworthiness of the issuer and the strength of the program or underlying investment. While these programs may offer higher potential returns, they are also riskier because there is no security or backup in case the program fails or experiences losses.

Key Features of Non-Collateral-Based PPPs:

- Higher Risk: Without collateral, non-collateral-based PPPs are inherently riskier. Investors are entirely dependent on the program’s ability to deliver returns. If the investment underperforms or fails, there is no collateral to fall back on.

- No Asset Backing: Since there is no collateral, the investment is not supported by any tangible or physical assets. This can make non-collateral-based PPPs feel more speculative and less secure.

- Lower Minimum Investment: In many cases, non-collateral-based PPPs allow for a lower minimum investment compared to collateral-based programs, making them more accessible to a wider range of investors. This can be appealing to smaller investors, though it comes with the trade-off of higher risk.

- Potential for Higher Returns: With higher risk generally comes the potential for higher returns. Non-collateral-based PPPs may offer more lucrative returns due to the speculative nature of the investment and the lack of backing assets.

How It Works:

Benefits:

- No Initial Capital Outlay for Collateral: Investors do not have to lock up additional assets to participate.

- Accessibility: Non-collateral-based programs can be more attractive to a wider range of investors since no physical asset is needed.

Risks:

- Higher Risk Exposure: Without collateral, there is no backup security if the program fails, leading to a complete loss of investment.

- Higher Risk Exposure: Without collateral, there is no backup security if the program fails, leading to a complete loss of investment.

Example of a Non-Collateral-Based PPP:

If you invest $100,000 into a non-collateral-based PPP, you’re fully relying on the program’s ability to produce high returns. There’s no collateral to secure the investment, so if the program fails, you risk losing the entire amount.

Collateral-Based vs. Non-Collateral-Based PPPs: Key Differences

When to Choose Collateral-Based PPPs

- Risk-Averse Investors: If you’re an investor who values security and wants to minimize risk, a collateral-based PPP is likely the better choice. The collateral provides a safety net in case the program doesn’t perform as expected.

- Larger Investments: If you have significant capital to invest and want a more secure investment with reduced risk, collateral-based programs are generally more suitable.

- Long-Term Stability: If you’re looking for a more stable and predictable investment, the additional protection offered by collateral-based PPPs can make them a more appealing option.

When to Choose Non-Collateral-Based PPPs

- Risk-Tolerant Investors: If you are willing to take on higher risk for the possibility of higher returns, a non-collateral-based PPP might be a good fit. However, be prepared to lose your investment if the program fails.

- Smaller Investments: If you want to invest a smaller amount or test out the investment program, non-collateral-based PPPs usually have lower minimum investment requirements, making them more accessible.

- Seeking High Returns: If the goal is to target higher returns, non-collateral-based PPPs might offer more aggressive strategies that could yield larger profits—albeit with greater risk.

Conclusion

Both collateral-based and non-collateral-based Private Placement Programs (PPPs) offer unique benefits and risks. Collateral-based PPPs provide additional security through the backing of tangible assets, making them more suitable for investors seeking stability and risk mitigation. On the other hand, non-collateral-based PPPs offer higher potential returns but come with greater risk, as there’s no asset to secure the investment.

Choosing between these two types of PPPs ultimately comes down to your investment goals, risk tolerance, and the level of security you want in your investment. Be sure to conduct thorough research and consider consulting a financial advisor to ensure that your choice aligns with your financial strategy and risk profile.